| Home Heating in the USA: A Comparison of Forests with Fossil Fuels | The Oil Drum | DrumBeat: December 15, 2007 |

| The Earth and Energy Round-Up: December 12th/15th 2007 | The Oil Drum: Canada | The Finance Round-Up: December 19th 2007 |

The Finance Round-Up: December 14th 2007

Posted by Stoneleigh on December 15, 2007 - 4:43pm in The Oil Drum: Canada

World bankers resort to firebreak

Never before have the central banks of North America, Europe, and Britain, acted together as such a unified phalanx, but never before have transatlantic credit markets seized up with such violent effect.

"This is a drastic action. The central banks want to place a fire-break to stop credit tensions spilling over into the broader markets and becoming the catalyst for a global economic crunch," said Ian Stannard, an economist at BNP Paribas.

While yesterday's joint move was sketched at the G20 a month ago, and fine-tuned in encrypted telephoned calls over the past month, the final trigger seems to have been the spike in the crucial three-month money rates that lubricate finance. Dollar and sterling Libor spreads have vaulted in recent days. Euribor spreads reached an all-time high of 99 yesterday morning....

...."There's a real danger that this may not work. Both the Fed and the ECB have injected a lot of liquidity before, but the banks are hoarding it. We're still seeing all the signs of stress with Libor and the VIX [fear gauge] at very elevated levels. The reason is that people still don't know where the bodies are buried," he said. "This may be a Made-in-America credit crisis but the Americans have cleverly exported their sub-prime cancer to pension funds all over the world. The risk now is a recession on both sides of the Atlantic," he said.

Fed teams with central banks on credit

"Clearly, the Fed is feeling its way in the dark here. Current conditions are unprecedented in modern times," said Ian Shepherdson, chief U.S. economist at High Frequency Economics.

Analysts said the use of auctions to try to get more money into the banking system was an acknowledgment that efforts to spur direct loans from the Fed to banks through the Fed's discount window had not worked as well as hoped because of banks' fears that investors could become worried if they started utilizing the Fed's discount window to any large extent.

In its announcement, the Fed said it had reached an agreement with the European Central Bank as well as the Bank of England, the Bank of Canada and the Swiss National Bank to address what it termed "elevated pressures" in credit markets....

....The first auction of $20 billion was scheduled for next Monday, followed by another auction of $20 billion on Dec. 20. The third and fourth auctions will be on Jan. 14 and 28 with the amounts not yet set.

The Fed said that the new auction process should "help promote the efficient dissemination of liquidity" when other lines of credit were "under stress."

Fed, ECB, Central Banks Work to Ease Credit Crunch

The Federal Reserve, European Central Bank and three other central banks moved in concert to alleviate a credit squeeze threatening global growth, in the biggest act of international economic cooperation since the Sept. 11 terrorist attacks.

The Fed said in a statement it will make up to $24 billion available to the ECB and Swiss National Bank to increase the supply of dollars in Europe. The Fed also plans four auctions, including two this month that will add as much as $40 billion, to increase cash in the U.S.

Central bankers took the action after interest-rate reductions in the U.S., U.K. and Canada failed to allay concerns that banks will reduce lending, which may send the U.S. into recession and hobble growth abroad. Borrowing costs have climbed as mounting losses on securities linked to subprime mortgages caused lenders to conserve cash.

``This is shock and awe,'' said Fred Goodwin, a fixed- income strategist at Lehman Brothers Holdings Inc. in London. ``The fact that it's coordinated means they have joined together in the war to attack the problem, which is that banks don't trust each other.''

Central banks unite to avert market turmoil

Central banks in Europe and North America unleashed a powerful and rare arsenal of liquidity measures Wednesday meant to stave off the threat of a steep deterioration in credit conditions over Christmas.

But analysts fear the measures will only delay the inevitable balance sheet pain and market turmoil that is necessary to purge shaky debt securities from global markets. And Bank of Canada Governor David Dodge conceded he was unsure the measures would have a lasting effect.

“It's very unusual. But it's also very unusual to see all the world's banks at such risk,” said Sherry Cooper, chief economist at BMO Nesbitt Burns Inc.

“They wouldn't be doing this if they didn't know this situation is very serious.”

As markets opened yesterday morning, the Bank of Canada announced that it had co-ordinated with the U.S. Federal Reserve, the European Central Bank, the Bank of England and the Swiss central bank to deepen the pool of short-term lending available over the end of the year, and make it more accessible.

“It was quite clear that there were a lot of worries about year-end and about the valuation … of assets on banks' books over this year-end,” Mr. Dodge explained in an interview.

“This could mean that financial markets, which had been volatile and not functioning all that well anyway through the course of the fall, could become even more volatile and less functional over this period of the uncertainty.”

But all in all, there is a stigma attached to borrowing from the Fed through the discount window: the banks have to disclose it and it illustrates severe financial weakness to their shareholders and depositors. For example, one source of liquidity that banks and companies like Countrywide (CFC) have been using is the Federal Home Loan Bank system where they don’t really have to tell anyone. This has saved the banking system so far but is tapped out.

So the Fed is considering a “new auction system”. Essentially, what the Fed is doing is taking the stigma away from the discount window--the Fed will lend directly to banks and the banks don’t have to tell anybody. Theoretically, the Fed could make these quiet loans for indefinite periods, thus giving banks more permanent capital (it’s really credit, but banks call it capital)....

....The plan won’t work. Under the repo/fractional reserve system the debt can be hidden because it is spread out among many banks. The Fed lending $10 billion (and thus their balance sheet rising by $10 billion) will turn into $500 billion as other banks lend that money out and only keep a fraction of it for themselves. This is not working. Under the “new” plan the Fed will lend directly to each bank. If they want to create $500 billion of new credit the Fed’s balance sheet will increase $500 billion.

Fed Knowingly Takes Suspect Collateral in TAF Program

In Global Coordinated Panic we discussed actions being taken by the Fed, Bank of Canada, the Bank of England, the European Central Bank, and the Swiss National Bank to address "elevated pressures in short-term funding markets".

One of the actions by the Fed was the establishment of a Term Auction Facility (TAF) program, whereby the Federal Reserve will auction term funds to depository institutions against a wide variety of collateral that can be used to secure loans at the discount window.

Of course the Fed wants this all kept a secret so it will not disclose who is going to this special window. In addition, (and not that this is any kind of surprise) but the collateral the Fed is willing to take for these temporary loans is rather suspect to say the least. It turns out the Fed Is Using Very Old Valuations For The Term Loan Facility Auction.

Derivative Trades Jump 27% to Record $681 Trillion

Derivatives traded on exchanges surged 27 percent to a record $681 trillion in the third quarter, the biggest increase in three years, the Bank for International Settlements said.

Interest-rate futures, contracts designed to speculate on or hedge against moves in borrowing rates, led the increase with a 31 percent increase to $594 trillion during the three months ended Sept. 30, the Basel, Switzerland-based BIS said today in its quarterly review. The amounts are based on the notional amount underlying the contracts.

Trading surged as investors bet on losses linked to record U.S. mortgage foreclosures and policy changes by the Federal Reserve and the European Central Bank to offset the credit slump. The Fed cut its benchmark interest rate by half a point to 4.75 percent in September, the central bank's first reduction in four years.

``The turbulence in financial markets led to the busiest trading on record,'' BIS analysts Ryan Stever, Christian Upper and Goetz von Peter wrote in the report.

Mish: Derivatives Trade Soars To Record $681 Trillion

Already banks no longer trust each other and/or are so capital impaired they cannot or will not lend to each other overnight. Washington Mutual is the latest casualty in that regard.

Now we find out that there appears to be a growing suspicion about the possibility of counterparties defaulting on derivative deals. Given that derivatives are ten times the global economy that suspicion sure seems justified....

....I have a failsafe prediction: Several hedge funds are going to get carted out on a stretcher all at once and cause a cascade of defaults. Many hedges are in place that are based on other counterparty hedges paying off in the event of "an event". When "the" event comes, those hedges will prove to be worthless.

Long Term Capital Management (LTCM) will look like a picnic in the park compared to the derivatives mess we are currently building up. For more on LTCM and the inherent systemic risks of leveraged derivatives please see Genius Fails Again.

Global economy is exposed to America’s houses of cards

It is one thing to borrow to make an investment, which strengthens balance sheets; it is another thing to borrow to finance a vacation or a consumption binge. But this is what Alan Greenspan encouraged Americans to do. When normal mortgages did not prime the pump enough, he encouraged them to take out variable-rate mortgages - at a time when interest rates had nowhere to go but up.

Predatory lenders went further, offering negative amortization loans, so the amount owed went up year after year. Now reality has hit: Newspapers report cases of borrowers whose mortgage payments exceed their entire income.

Globalisation implies that America’s mortgage problem has worldwide repercussions. America managed to pass off bad mortgages worth hundreds of billions of dollars to investors (including banks) around the world. They buried the bad mortgages in complicated instruments, buried them so deep that no one knew exactly how badly they were impaired, and no one could calculate how to re-price them quickly. In the face of such uncertainty, markets froze.

Those in financial markets who believe in free markets have temporarily abandoned their faith. While the US Treasury and the International Monetary Fund warned East Asian countries facing financial crises 10 years ago against the risks of bailouts and told them not to raise their interest rates, the US ignored its own lectures about moral hazard effects, bought up billions in mortgages, and lowered interest rates.

But lower short-term interest rates have led to higher medium-term rates, which are more relevant for the mortgage market.

Falling into the liquidity trap

We learned this in the 1930s, when, after first shrinking the money supply enough to pull prices down by about 25%, the Federal Reserve of that era tried to force-feed liquidity into the economy with the hopes of pushing it out of its slump. It didn't work. Lenders were reluctant to lend, while potential borrowers did not want to borrow.

Banks were struggling under mountains of loans gone sour and were in no frame of mind to throw good money after bad. For their part, most firms were not willing to assume new debts, since falling sales and earnings led them to conclude that there was little productive use they could make out of these borrowed funds. The great economist John Maynard Keynes dubbed this phenomenon a "liquidity trap." It was perhaps the first realization that the Fed's powers were not as great as previously thought....

....This is because the markets lack confidence. As I wrote two weeks ago, "fear, and not a lack of liquidity, is what's freezing up the credit markets ... and ... it's going to take a lot more than infusions of liquidity to thaw them." You know that fear is stronger than greed these days when banks refuse to lend to each other - never mind to businesses or to consumers.

All Canadians could pay a price if banks fail to come up with an agreement to save the troubled sector of the country's debt market and $300-billion worth of leverage is allowed to unwind in a worst-case scenario, David Dodge, governor of the Bank of Canada, said yesterday....

....The non-bank ABCP market seized up during the August liquidity crisis amid fears the complex derivatives were tainted by defaulting U.S. sub-prime mortgages. Players in the market agreed to voluntarily freeze dealings and work out a bail-out that would prevent a fire sale of the assets.

Led by chairman Purdy Crawford, the bailout --known as the Montreal Accord -- is due to be completed by Friday.

Mr. Dodge said the dangerous aspect of ABCP is leverage, which can multiply losses.

"Because they're levered, the amount of global assets that would be affected if all this went down would be eight or 10 times the nominal value of the notes, so you're starting to get into the $200-billion, quarter-trillion-dollars' worth," Mr. Dodge said.

"So everybody, including the international banks, have a real interest in trying to somehow get this thing resolved because if these go down and a whole pile of SIVs [Structured Investment Vehicles] elsewhere go down, then you've got an immense number of these assets being dumped on the market at the same time."

ABCP proposal to offer range of losses

The committee seeking to revive $33-billion of stranded asset-backed commercial paper (ABCP) will propose that investors shoulder a range of losses under a restructuring to be unveiled by the end of the week.

The group is on track to work out an exchange of the troubled short-term notes for new classes of healthier, long-term notes, according to people close to the discussions. The proposal calls for a multistep process where most of the frozen notes will be swapped for new floating-rate bonds with maturities of up to nine years.

How much investors get back will depend on valuations that the committee's adviser, J.P. Morgan Securities, has assigned to dozens of series of ABCP.

It is understood that the range of writedowns will vary dramatically according to the current market value of mortgages, leases and other financial products underlying ABCP. The most troubled paper was issued by a small handful of trusts such as Apsley Trust, which sources said faces losses of as much as 50 per cent because of its heavy exposure to a toxic class of U.S. mortgages known as subprime. Significantly smaller losses are expected for the bulk of the frozen ABCP because they are backed by conventional mortgages or complex derivatives that are still generating income.

S&P begins rating Canadian ABCP

Standard & Poor’s, which did not previously cover Canadian ABCP, Tuesday assigned a top rating to a new paper program from Deutsche Bank, called Okanagan Funding Trust. Like other flavours of ABCP, Okanagan will sell short-term paper secured against a collection of auto loans, equipment leases and mortgages.

S&P had not been rating these ABCP programs out of what proved to be well-founded concerns about the liquidity backstops, or guarantees that investors would get paid out if the paper couldn’t be rolled over. Rival agency DBRS did rate this debt, and $32-billion of non-bank-issued ABCP ended up frozen in August when buyers walked away, and banks refused to backstop the paper. ABCP issued by the major Canadian banks, which dominate this market, continued to roll over this summer.

The game of point-the-finger begins in ABCP mess

When two Vancouver businessmen quietly filed a pair of lawsuits against Canaccord Capital Corp. this fall, they had good reason to believe that the matter would be privately settled.

In separate claims filed with the Supreme Court of British Columbia, the men alleged that Canaccord and some of its brokers misrepresented asset-backed commercial paper (ABCP) as guaranteed investments. One, building contractor Robert Madiuk, claimed his Canaccord broker had promised in writing that the short-term notes were guaranteed by a major Canadian bank. The other, junior mining executive Gregory Hryhorchuk, alleged his broker promised "no downside risk."

The men alleged their Canaccord brokers purchased a total $273,000 of ABCP for their accounts without their approval in early August. The purchases were made in the rocky final days when panicky investors fled the short-term notes and left $34-billion of ABCP stranded.

When the cases landed on the desk of Forstrom Jackson LLP lawyer Patricia Taylor in September, she would have been justified in concluding that the facts and the relatively small size of the claims would prompt Canaccord to settle the dispute to avoid negative publicity.

Canaccord, however, made no settlement overtures. Instead, it chose to defend itself by pointing the finger of blame at one of Canada's largest banks, ensuring that the lawsuits would get the media coverage they did last week. In what is known as a third-party notice, Canaccord entangled the Bank of Nova Scotia in the two lawsuits by alleging that the bank had negligently and knowingly dumped troubled ABCP on the brokerage, which was vulnerable because of its "lack of special experience, expertise and information" about the very notes it was pitching to its customers.

Fed's Expected Cut Spurs Shoulda-Woulda-Couldas

Bianco says press stories in the last two weeks had heightened expectations that ``something else was coming,'' that the Fed would try to address elevated Libor rates, or the rate at which banks borrow from one another overseas. Libor (for London interbank offered rate) serves as a benchmark for many short-term loans, including adjustable-rate mortgages.

The Fed can pretty much put the overnight rate where it wants, and Libor generally follows.

Not in recent months. The funds rate is 100 basis points lower than it was in September, yet three-month Libor has fallen by only 25 basis points, reflecting a generalized unwillingness to lend. At 86 basis points, the spread between the two rates is the highest in seven years....

....Maybe all the disappointment was just a dose of reality creeping in. Investors are looking for the magic bullet that would make everything OK, encourage banks to lend (a lower rate would help), heel the wounds in the home-loan market, wipe away the accumulated debt of consumers and put the economy back on track.

Alas, there is no such tool in the Fed's arsenal.

Of course, that credit regime was so loose that we now have $5 or 10 trillion worth of new debt on the US consumer, not to mention all the rest of the West, the UK figures here, and all the rest of the West.

Now that we see weekly deterioration of world credit markets, like this week, Societe bank in France taking on $ 4 billion of bad SIVs because they were about to be forced into a fire sale, HSBC taking $20 billion of more bad mortgage derivatives onto their books, too last week or so, Banks bailing out their money market funds, (at least so far) lest panic flight appears, like the Florida mess, BoA freezing a big fund this week from withdrawals.

Central banks lowering interest rates to combat the freezing CP markets, the rising Libor rates that determine what US ARMs reset to… the US Fed and ECB putting out so far $1 trillion in emergency financial market liquidity since August – in my estimation.

We are on the verge of a gigantic world financial deleveraging.

Libor, a key rate for Joe Ultra Light Sixpack, barely budged following the latest “liquidity” gambit from the Fed and other central banks. It currently checks in around 5.10%. This is important not only as a measure of interbanking confidence, but also because so many problematic toxic mortgages are tied to it.

A recent report from the Federal Reserve Bank of New York shows that the six-month Libor rate will determine the reset rates for an estimated 99% of subprime ARMs and 38% of Alt-A ARMs in the U.S. that have been securitized. A further 1% of subprime ARMs and 22% of Alt-A ARMs will reset based on the one-year Libor rate. Alt-A is a category between prime and subprime that often involves borrowers who don’t fully document their income or assets. About half of student lenders peg their private, variable-rate student loans to Libor.

The Issue is Solvency Not Liquidity

Market observers continue to be confused about what they are falsely calling “liquidity problems”. As interbank rates like the Libor (quoted at 5.20% this morning) continue to fail to respond the central bank rate cuts, any thinking person ought to be able to connect the dots as to why. The reason: essentially no one is willing to make loans to dead men walking, or even the walking wounded at nominal low rates any more. The very definition of Ponzi finance is the borrowing of new funds to pay debt service on old debt that normal income does not support. Most lenders aren’t interested in unsound lending right now.

Despite this clear implication, the Fed grasps for new smoke and mirrors to provide a source of funds (called liquidity by the spinmeisters) so that lenders can continue to float bad loans. The latest looks like the Fed will get into the loan auction funding business. This in effect will allow lenders to bring fictitious capital to the table for low interest loans in which to buy the fictitious capital of other players.

In past financial crises — the stock market crash of 1987, the aftermath of Russia’s default in 1998 — the Fed has been able to wave its magic wand and make market turmoil disappear. But this time the magic isn’t working.

Why not? Because the problem with the markets isn’t just a lack of liquidity — there’s also a fundamental problem of solvency.

Let me explain the difference with a hypothetical example.

Suppose that there’s a nasty rumor about the First Bank of Pottersville: people say that the bank made a huge loan to the president’s brother-in-law, who squandered the money on a failed business venture.

Even if the rumor is false, it can break the bank. If everyone, believing that the bank is about to go bust, demands their money out at the same time, the bank would have to raise cash by selling off assets at fire-sale prices — and it may indeed go bust even though it didn’t really make that bum loan.

And because loss of confidence can be a self-fulfilling prophecy, even depositors who don’t believe the rumor would join in the bank run, trying to get their money out while they can.

But the Fed can come to the rescue. If the rumor is false, the bank has enough assets to cover its debts; all it lacks is liquidity — the ability to raise cash on short notice. And the Fed can solve that problem by giving the bank a temporary loan, tiding it over until things calm down.

Matters are very different, however, if the rumor is true: the bank really did make a big bad loan. Then the problem isn’t how to restore confidence; it’s how to deal with the fact that the bank is really, truly insolvent, that is, busted.

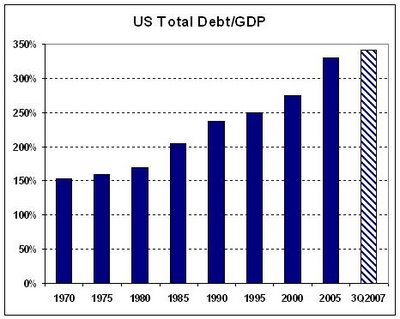

The main concern today is fiduciary adequacy and not liquidity. We have already borrowed so much (total debt is near 350% of GDP) that our ability to service existing debt is more relevant than access to additional debt. The importance of the Fed to the economy is thus limited, and our fixation with what it does, or does not do, is a distraction from dealing with the real issues.

What are the issues?

- Forget the Fed; there can be no monetary solutions to fiduciary problems.

- Re-establish the relevance of fiscal policy as more than just discussion about tax cuts.

- Raise earned income, instead of relying on capital gains and portfolio income; create permanent high value-added jobs, targeted to exports.

- De-leverage.

- Emphasize industry over finance and production over consumption.

Alan Greenspan: The Roots of the Mortgage Crisis

On Aug. 9, 2007, and the days immediately following, financial markets in much of the world seized up. Virtually overnight the seemingly insatiable desire for financial risk came to an abrupt halt as the price of risk unexpectedly surged. Interest rates on a wide range of asset classes, especially interbank lending, asset-backed commercial paper and junk bonds, rose sharply relative to riskless U.S. Treasury securities. Over the past five years, risk had become increasingly underpriced as market euphoria, fostered by an unprecedented global growth rate, gained cumulative traction....

....The crisis was thus an accident waiting to happen. If it had not been triggered by the mispricing of securitized subprime mortgages, it would have been produced by eruptions in some other market. As I have noted elsewhere, history has not dealt kindly with protracted periods of low risk premiums.

Commercial Paper Rates and Outstanding

Calculated Risk comment: Worse than August. Worse than 9/11.

Crisis seen ending when distressed market buys

Many asset managers, like F&C Partners, are poised to snap up crisis-hit assets at deep discounts. Such demand could restore liquidity to the credit market, but it comes at prices that banks and other holders are not yet prepared to accept. "The problem is that if they write it down, then they are going to take a capital hit, their equity will be reduced and they will have to reduce the size of their balance sheets. They are stuck in a bind, clogged up," Culligan said.

"Whether it's banks, insurance companies, SIVs, conduits, basically the asset sides of a number of large balance sheets have shrunk to the point where it has seriously impaired or wiped out the equity."What needs to happen is an injection of equity, and the eventual sources of that equity are likely to be in the Middle East or Far East, he said. On Monday, Swiss bank UBS announced a $10 billion writedown and said it had obtained a capital injection of 13 billion Swiss francs ($11.5 billion) from a Singapore government entity and an unidentified Middle East investor.

UBS says Singapore investment 'first step' in reorganisation

UBS said Tuesday that the decision by Singapore's state investment arm to inject nearly 10 billion dollars in fresh capital is just the "first step" in a major reorganisation of the Swiss bank's activities.

UBS turned to the Government of Singapore Investment Corporation (GIC) to plug a 10-billion-dollar (6.8-billion-euro) hole caused by losses in the US mortgage crisis. These losses, coming on top of a 4.2-billion-Swiss franc (3.7-billion-dollar, 2.5-billion-euro) writedown announced in October, are the result of "a small group of people in investment banking," UBS chairman Marcel Ospel told an investor day in London. UBS will now move to "reposition its fixed revenue activities," Ospel said....

....UBS also said that a strategic investor in the Middle East, which it did not identify, is injecting an additional two billion francs into the bank. Ospel said that both these moves were "long-term" investments.

It is awkward, to say the least, for the West to complain when Asian and Middle Eastern government-owned investment pools shore up capital-starved banks that are vital to the world economy. It is like running out of gasoline in the middle of nowhere and being picky about who drives by with spare fuel. And the U.S. economy needs about $2 billion every day from foreigners to keep it going. It gets this money by borrowing or by selling off chunks of assets like Citigroup or Bear Stearns.

Even without counting the vast reserves of Asian central banks, sovereign-wealth funds, or SWFs -- an abbreviation once more common to personal ads than news columns -- today have about $3 trillion in assets and are on their way to $12 trillion by some estimates. They are bigger than hedge funds and private-equity firms combined, though those outfits magnify their clout with lots of borrowed money. And they pose at least three risks:

The first worry is backlash. Americans, with some trepidation, accept foreign investment in the U.S. -- especially when it comes in the form of jobs making Toyotas or price-reducing competition for cellphone service from Germany's T-Mobile. But the 2006 explosion over the proposed purchase by Dubai Ports World of operations of several U.S. ports single-handedly raised barriers for foreign direct investment around the world. It is a reminder how much anxiety there is about globalization and how quickly politicians can respond.

SIVs Shrink, Easing Concerns About Fire-Sale, Rescue

Devised by former Citigroup bankers Stephen Partridge-Hicks and Nicholas Sossidis in 1988, SIVs aim to profit by borrowing at least 10 times the initial funding provided by long-term capital or income noteholders. The money is invested in hundreds of securities from asset-backed debt with AAA credit ratings to bank bonds. Mortgage debt made up 23 percent of SIV assets, with most having no direct subprime link, Moody's said in July.

Capital noteholders, who are first in line for losses, received annual returns from 2 percentage points to 2.75 percentage points more than benchmark interbank rates, based on a Moody's survey in 2005.

SIVs profit by using top credit ratings to borrow at low short-term rates. The model had broken down by September when money market investors either stopped buying SIV debt or charged as much as 6.3 percent on 30-day asset-backed commercial paper, the highest rate in more than six years. SIVs were left paying more to borrow than they were earning, Moody's said in a report in September.

``The market is being divided into two camps,'' said Tawadey at BNP Paribas. ``We are seeing a polarization between the banks that have the strength to support their SIVs and take up some of the implicit obligations, and some of the U.S. institutions that are already facing other pressures, such as higher credit card delinquencies and subprime losses.''....

....Citigroup's ``outsized'' investment in SIVs and collateralized debt obligations, bonds based on underlying assets, puts the biggest U.S. bank in a ``precarious position'' that may trigger a breakup or merger with a competitor such as JPMorgan, CreditSights Inc. in New York said in a Dec. 9 report.

Citigroup offloads assets from SIVs

Citigroup has slashed the size of its struggling off-balance-sheet investment funds by more than $15bn in two months through quiet side deals with some junior investors, according to people familiar with the business.

The news that the troubled US bank has been finding ways to offload assets from its structured investment vehicles (SIVs) without resorting to fire sales comes as Société Générale on Monday became the latest bank to announce a bail-out for its own $4.3bn vehicle. SocGen's decision follows similar moves by HSBC, Standard Chartered and Rabobank in the past fortnight.

Citigroup to Assume Control of SIVs

Citigroup Inc. said Thursday it plans to assume control of the seven "structured investment vehicles" the bank advises to help them repay their debts. Citigroup will provide a "support facility" for its seven SIVs with investments totaling $49 billion and incorporate them onto its balance sheet. The bank previously said it had no plans to bring the SIVs onto its books.

SIVs are complex investment funds established by banks like Citigroup and sold to investors. SIVs borrow money by selling short-term debt like term notes and commercial paper, then using the borrowed money to buy bank, mortgage and credit card debt that yield higher returns.

The funds profit off management fees and the spread between how much they collect on the investments and how much it costs them to borrow.

SIVs jumped to the forefront of this year's credit crisis when many of the investments they held, particularly mortgage investments, lost a lot of value as demand for risky debt shriveled.

This triggered concern that lenders would be unwilling to keep lending to SIVs. The viability of a SIV hinges on its ability to continue borrowing short-term money. If it is unable to renew loans, it has to find new sources of cash or liquidate its investments to repay lenders.

Moody's Investors Service and Standard & Poor's -- two of the three major credit-rating agencies -- were considering downgrading the ratings on several of the world's roughly 30 SIVs, including the seven Citigroup created.

Citigroup will bring the SIVs onto its balance sheet in order to protect their credit ratings and give them time to sell their assets, the bank said.

CIBC's Big Subprime Secret Might Cost Billions: Jonathan Weil

Canadian Imperial Bank of Commerce has a big skeleton in its vault. And the bank's executives are doing a ham-handed job of trying to keep it there.

CIBC's lightly guarded secret is the name of a ``U.S. financial guarantor'' that faces a possible downgrade on its A credit rating and is ``not necessarily rated by both Moody's & S&P.'' That's how CIBC last week described the company that is insuring $3.47 billion, or about a third, of the collateralized- debt obligations it holds that are tied to U.S. subprime mortgages.

The company's identity matters because the bank said these hedged CDOs were worth just $1.76 billion at Oct. 31, down almost half from their face amount. If the guarantor goes poof, CIBC loses its hedge on these derivative contracts. And the Toronto-based bank would have to recognize the loss, which is growing.

All the King´s Horses or Rearranging the Deck Chairs on the Titantic?

Essentially, we can assume MBIA is on super-secret probation,’ said Rob Haines, an analyst with CreditSights. Michael Cox, securitisation analyst at RBS in London, said the next two weeks would be a critical period… ‘[These companies] have become the focus for those searching for the next domino to fall as the credit crisis unfolds,’ he said. MBIA insures just over $1,000bn of municipal and structured finance bonds. However, it only had the ability to pay $14.2bn of claims as of September 30.

Washington Mutual Will Take $1.6 Billion Writedown

Washington Mutual Inc., the biggest U.S. savings and loan, will write down the value of its home- lending unit by $1.6 billion in the fourth quarter and cut about 6 percent of its workforce as mortgage-market losses increase.

Washington Mutual, led by Chief Executive Officer Kerry Killinger, also slashed its quarterly dividend to 15 cents a share from 56 cents and forecast a loss for the quarter, according to a statement yesterday from the Seattle-based bank. Provisions for bad loans will be $1.5 billion to $1.6 billion, more than the $1.3 billion the company previously predicted. It plans to shutter 190 of 336 home-loan centers.

Fitch Ratings and Moody's Investors Service Inc. lowered Washington Mutual's credit rating, citing the firm's deteriorating mortgage assets. The bank has lost 56 percent of its market value this year, the worst performance in the 24- member KBW Bank index, amid declining U.S. housing prices and record home loan delinquencies. Washington Mutual said it plans to sell $2.5 billion of convertible stock to shore up capital.

``They're clearly concerned the industry will stay in a negative mode for an extended period,'' said Richard Bove, an analyst at Punk Ziegel & Co. in Lutz, Florida. ``The fact they're laying off so many people indicates they're concerned this is not just a one-time event.''

Freddie Mac expects $10-12 billion credit losses

Freddie Mac expects to see credit losses of $10 billion to $12 billion on the book of mortgages it currently owns, the mortgage finance company's chief executive said on Tuesday....

....In the coming months, Syron said, the public will increasingly see the distressing public face of massive foreclosures and that could imperil the entire economy.

"We have seen a ton of foreclosures but we have not seen a lot of pictures of people standing in front of their house with their furniture on the front lawn saying 'What am I going to do?" he said.

"As that starts to happen, and it will happen, I am afraid of the impact that this has," he said, citing a risk that a public concern over the housing market could curtail consumer spending.

Subprime-hit German banks search for partners

The owners of battered German lender WestLB emerged from crisis talks on Wednesday saying that they would be happy to sell a stake in their subprime-hit bank.

The comments are the latest sign of the worsening condition of German banks in the wake of the subprime storm.

Earlier, the state of Saxony, which owns rival lender SachsenLB, said it hoped to sign a deal to sell the stricken bank to a rival despite a row over who pays for the bank's dud investments in subprime mortgages.

Last week, WestLB warned that the crisis in financial markets was getting worse as it skidded into the red and said 2007 losses would mount to hundreds of millions of euros.

German Investor Confidence Decline to 15-Year Low

Investor confidence in Germany dropped more than economists forecast in December, reaching the lowest level in almost 15 years, as rising credit costs dimmed the outlook for economic growth....

....The cost of borrowing euros for three months rose to the highest since December 2000 today as banks hoarded cash to cover their commitments over year-end.

The euro interbank offered rate, the amount banks charge each other for such loans, rose 3 basis points to 4.93 percent, the European Banking Federation said today. That's 93 basis points more than the European Central Bank's benchmark rate

The slump in global credit markets may force banks, brokerages and hedge funds to cut lending by $2 trillion and trigger a ``substantial recession'' in the U.S., Goldman Sachs Group Inc. forecast on Nov. 16.

Northern Rock takes $574-million credit hit

Northern Rock said it had taken a £281-million ($574 million) hit, or two-thirds of its market value, from its exposure to the credit crisis, adding to its woes as it brought in a new chief executive....

....Northern Rock is being auctioned off by its advisers after it became Britain's highest profile casualty of the credit crisis, but the future of that process has been thrown into doubt in recent weeks, with two suitors withdrawing....

....Northern Rock said the £281-million writedown included a £118-million hit from its investment in structured investment vehicles (SIVs) and a further £32-million from its investment in the more highly leveraged SIV-lites.

HBOS pain takes UK bank writedowns to £2bn in a week

HBOS has become the fourth UK lender in a week to announce a multi-million pound writedown on the back of the turmoil in global credit markets, taking the total written off by UK banks in the last seven days to almost £2bn (€4bn).

The bank this morning said it wrote down £520m on its investments, three days after Lloyds TSB revealed a £200m hit on its own portfolio and a week after Royal Bank of Scotland reduced the value of its assets by £950m as a result of its exposure to US sub-prime.

Northern Rock continued to add to the woes of the UK banking sector, saying this morning it had written down its collateralised debt obligation portfolio by £281m.

HBOS was forced to take a the £520m charge against its £80bn portfolio of floating-rate notes and asset-backed securities.

Florida Fund Reduced By $1.9 Billion After SIV Losses

Managers of the Florida pool were willing to gamble local government money on SIV debt because they had the safest credit ratings and offered higher yields than other short-term fixed- income investments. Now, downgrades and defaults on those holdings have left schools and towns statewide without full access to cash they are accustomed to drawing upon for routine expenditures such as payroll for teachers and police.

``Who would invest in a fund that had the kind of risk they did?'' said Michael Geoghegan, chief financial officer at Broward County, which includes Fort Lauderdale.

Geoghegan pulled out the county's $200 million investment in the pool in mid-November after he learned the fund held SIV debt that had been downgraded below investment grade.

Florida says $9B can't be pulled from fund

Local governments will be able to withdraw no more than a quarter of the $12 billion they have invested in a Florida-run investment fund before next spring -- because the fund doesn't want to sell the investments at a loss.

Investing agencies, including many in Central Florida, also found out that at least $350 million of their cash is tied up in investments whose ratings are so low that their value "truly is a question mark," according to Simon Mendelson, a top manager with BlackRock, an investment firm hired by the state to salvage the pool. It won't be known until later next year -- when the investments mature -- whether they'll be worth anything, he added.

Mendelson spoke during a nearly two-hour conference call to representatives of hundreds of cities, counties, school boards and other agencies across Florida with money in the Local Government Investment Pool. He was joined by executives of the State Board of Administration, which until last week managed the fund.

Florida Official Seeks Probe of Investment Pool

Florida's top finance official asked for an investigation of policies that led the state's local government investment pool to invest in securities tied to the subprime mortgage market.

State Chief Financial Officer Alex Sink, in a letter yesterday to Florida's inspector general, Melinda Miguel, asked for a probe of whether the State Board of Administration's securities purchases violated its investment guidelines. Cities and schools withdrew $13 billion from the $27 billion fund last month after learning it held subprime-tainted debt that had defaulted or been downgraded.

Fed Forecasters Who Were Right See Funds Rate at 3.5%

The three most accurate forecasters of U.S. interest rates say the Federal Reserve will need to lower borrowing costs below 4 percent to prevent credit markets from seizing up.

UBS AG, Deutsche Bank AG and Dresdner Kleinwort were the only primary dealers of U.S. government securities to correctly forecast a year ago that the central bank would reduce its target rate for overnight loans between banks to 4.25 percent, according to a Bloomberg survey. The median estimate of the 22 firms was for a decline to 4.75 percent.

The economists now say policy makers will cut the target by at least another half percentage point because banks are raising costs for loans amid mounting losses from securities tied to subprime mortgages. The difference between the interest banks and the government pay for three-month loans, called the TED spread, rose to 2.21 percentage points yesterday from 1.59 percentage points on Sept. 18 when the Fed began lowering rates.

``The financial impact from subprime started off the chain reaction,'' said Maury Harris, chief U.S. economist in New York for UBS, Europe's biggest bank by assets. ``The decline in home prices was the genesis of everything that's happened,'' Harris said in a telephone interview. ``The economic impact is showing up now.''

Morgan Stanley issues full US recession alert

Morgan Stanley has issued a full recession alert for the US economy, warning of a sharp slowdown in business investment and a "perfect storm" for consumers as the housing slump spreads.

In a report "Recession Coming" released today, the bank's US team said the credit crunch had started to inflict serious damage on US companies.

"Slipping sales and tightening credit are pushing companies into liquidation mode, especially in motor vehicles," it said.

"Three-month dollar Libor spreads have jumped by 60 to 80 basis points over the last month. High yield spreads have widened even more significantly. The absolute cost of borrowing is higher than in June."

"As delinquencies and defaults soar, lenders are tightening credit for commercial, credit card and auto lending, as well as for all mortgage borrowers," said the report, written by the bank's chief US economist Dick Berner. He said the foreclosure rate on residential mortgages had reached a 19-year high of 5.59pc in the third quarter while the glut of unsold properties would lead to a 40pc crash in housing construction.

TD sees ‘significantly slower economic growth' as credit crunch bites

Problems in credit markets are more serious and more persistent than initially thought, and “the dominant economic theme for 2008 will be significantly slower economic growth in the United States, Canada and around the globe,” TD Bank economists said Thursday....

....In the United States, “we still don't believe that a recession is the most likely scenario, but the risks have become acute,” commented Mr. Alexander.

He added: “While there has been much talk about the ability of the global economy to decouple from a U.S. economic slowdown, this assumption is likely to be tested and debunked in the coming quarters.”

The combined actions of the world’s central banks on Wednesday smacks of a real fear that the world’s financial system is in trouble.

Injecting liquidity — that is lending money to banks — when short-term interest rates rise is perfectly normal in this age in which central banks target interest rates.

What is not normal is the Fed using auctions “to inject term funds through a broader range of counterparties and against a broader range of collateral than open market operations.” That move, the Fed says, “could help promote the efficient dissemination of liquidity when the unsecured interbank markets are under stress.”

Or, as a senior Fed official — that’s what the Fed wants him called — told reporters, “This is not about particular financial institutions, with particular problems. It is about market functioning.”

The New York state Attorney-General has sent subpoenas to banking giants after announcing an investigation into the sub-prime market crash. Banks are being charged with irresponsible lending after giving loans to people who would never be able to make repayments plus misleading investors over mortgage-backed securities....

....Mr Cuomo suggests that the banks creating the derivatives could be in trouble for failing in their legal obligation to ensure that prospectus information on the derivatives being sold was true.

Mortgage fix eluded lawmakers in 2001

The state of California had a chance to curb lending practices that would later contribute to a crisis in subprime mortgages when it set out in 2001 to regulate so-called "predatory" loans.

But lawmakers, many of whom took campaign contributions, trips to Hawaii and Rolling Stones concert tickets from subprime lenders, narrowed the legislation so much that consumer protections covered only a tiny percentage of mortgages, a review by The Bee found.

Saying they didn't want to dry up the market by being too restrictive, lawmakers produced a bill that let most lenders easily avoid making loans that triggered homebuyer safeguards.

Freezing Mortgages or Freezing the Real Estate Market?

The administration initiated a new plan to freeze introductory rates on subprime mortgages preventing them from resetting to higher rates for five years. However, there are some who believe that this plan focuses energy in the wrong direction.

Eli Tene, the President of I Short Sale, Inc., a leading nationwide loss mitigation service provider, believes that the freeze is just another sign that the administration does not have the necessary tools to deal with a crisis. "If the goal is to help distressed homeowners, the mortgage rate freeze is missing the target," says Tene.

Tene highlights four significant pitfalls in the plan that should be considered:

1. The plan is limited to loans made at the start of 2005 through July 30 of 2007, and will cover loans that had been scheduled to reset to higher rates between January 1, 2008 and July 31, 2010.

2. The plan targets only homeowners that are current in their mortgage payments. In other words, it ignores the growing number of homeowners who have already missed one or more payments. These homeowners continue to face foreclosure with no way out.

3. Freezing rates does not necessarily mean the rates will be low enough to allow the homeowner to stay current. Some mortgages have already adjusted and many of those who need to pay them cannot afford to do so.

4. The sheer notion that the housing market prices will increase, thus allowing homeowners to refinance their current adjustable rate mortgages does not hold water. On the contrary, the mortgage freeze will just assist the lackluster performance of the real estate market and will now lock both the property owner and the lender for a longer period of time.

The Capital of Slumping Home Sales

Many of those sales depended on adjustable-rate mortgages with tantalizingly low initial payments, and now that those mortgages are much harder to get, there aren’t many buyers willing and able to pay $500,000. Yet sellers in Paramount haven’t adjusted to the new reality by cutting their prices very much. Instead, the real estate market has frozen.

On Sunday, Luis Perez and his wife, Hilda, held their fourth open house since putting their apricot-colored stucco home on the market in August. They have reduced the price once, by about 5 percent. They still haven’t received a single offer.

Since the summer, only about three homes a week — including houses and condominiums — have sold in Paramount. In the third quarter of this year, only 30 homes changed hands, down from 134 in the third quarter of last year.

That 78 percent drop is bigger than the decline in any other ZIP code in the country, according to an analysis that a research firm called DataQuick Information Systems did for me. The biggest declines can generally be found in moderate-income towns on the outskirts of major metropolitan areas, where adjustable-rate mortgages had become the norm.

Ahead of the Bell: Mortgage Bill

A House committee is scheduled to vote Wednesday on legislation that would permit judges to shrink the size of home loans for bankrupt homeowners -- a mortgage-mess remedy supported by consumer advocates and ardently opposed by the lending industry.

Many Democrats say the proposal is a better way to help homeowners than a plan to freeze interest rates announced by the Bush administration last week and negotiated with lenders and investors.

Mortgage-industry leaders say the proposed legislation would open a floodgate of bankruptcy filings, further threatening the industry's already shaky footing. Lenders, they argue, would be forced to charge higher rates to offset any unpaid loan balances that would be reduced in court.

Foreclosures triple across region

"People are desperate," said real estate analyst Jack McCabe of McCabe Research and Consulting in Deerfield Beach, who has closely tracked the local decline.

"A lot of people weren't trying to buy a house over their means, but nevertheless they got caught up in this," he said. "Now they're emptying their savings, but for a lot of people it makes sense to cut their losses."

Indeed, tightened finance rules in the wake of the "subprime loan mess" plus a huge backlog of unsold homes on the market make it difficult for many cost-burdened homeowners to refinance with better terms, or to sell. In Palm Beach County, for instance, there's a four-year supply of homes for sale, according to Illustrated Properties Real Estate.

That leaves foreclosure as the last unhappy option for squeezed homeowners, as climbing rates in the Treasure Coast show.

Let's put it all together and attempt to answer the original question - when will the mighty US consumer shut off spending? The truthful answer is, I don't know. But I know where to look for very credible signs preceding the spending cuts: weekly jobless claims.I also know something even more important: given the hand-to-mouth existence, high debt and rising inelastic expenses, significant job losses will lead to deeper and faster spending cuts than ever before. That will be the critical point, not only for the consumer, but for the entire US economy.

The face of foreclosure: Tales of broken dreams

The lawmakers said they would propose a 90-day stay on foreclosures and a five-year stay on interest rate resets until the current foreclosure crisis subsides. The lawmakers also said they would support legislation to ban certain kinds of lending, including commissions that reward brokers for getting borrowers to pay more than they have to.

In Alameda County, 9,454 homeowners are in some stage of foreclosure this year. Either they have defaulted on their mortgages or received a notice of trustee sale of their home from the bank, according to statistics from the Home Mortgage Disclosure Act and the Housing and Economic Rights Advocate, based in Oakland.

The number of Alameda County homeowners receiving notices of default — meaning 90 days past due — on their mortgages soared 50 percent in the first nine months of 2007 over the same time last year. Such notices stand a good chance of evolving into foreclosure.

A long, cold winter in store for the poor

Virtually everyone is shuddering this year at the high cost of home heating oil.

Worst off are low-income families, who face heating-oil prices anywhere from 10 to 22 percent higher than last winter with less assistance from the federally funded Low-Income Home Energy Assistance Program. While the Bush administration falls down on the nation's moral responsibility to care for its poor and vulnerable, a few local souls are striving to make sure no families go without heat this winter.

Will the Free Market Kill Suburbia?

I wonder how much of the $6.3 trillion market for home loan bonds represents the failure of suburban sprawl as an economic engine for the US economy. Sprawl is the unsustainable growth model that bond investors are fleeing as if their hair were on fire. What an irony it would be, if the free market kills suburbia.

Far from being what the market wants, sprawl is a Ponzi scheme that depended on the securitization of mortgages into pools mixing form, content and risk into an unrecognizable hash. It was great bait--"what the market wants"--until the trawler nets came up empty.

A complete analysis of what percentage of subprime trouble is represented by low density, scatter housing has not been published. By 2005, this much is clear: the multi-billion dollar market for production homebuilders had been saturated. Mortgage brokers stimulated by egregious compensation practices were fishing in the final pool that had not dried up: prospects who could scarcely afford to rent, much less buy a home.

True to form, the fine print on those hundreds of billions of sprawl-linked bonds did not include anything like the true costs of sprawl: aquifers destroyed to plow more production homes on poor topsoil, wetlands gobbled up at a fearsome rate, putting drinking water supplies for whole cities at risk, not to mention the role of gas-guzzling automobiles as an priori condition of long commutes from tract housing to places of work.

The Growth Machine in the United States depends on the externalization of true costs and on bond buyers being agnostic. All that mattered was the assurance of ratings agencies and bond insurance to cover any unforeseen damages.

Personnel

Archives

- December 2008 (1)

- October 2008 (1)

- July 2008 (2)

- June 2008 (2)

- May 2008 (6)

- January 2008 (2)

- December 2007 (8)

- November 2007 (9)

- October 2007 (11)

- September 2007 (14)

- August 2007 (14)

- July 2007 (10)

- June 2007 (9)

- May 2007 (11)

- April 2007 (9)

- March 2007 (11)

- February 2007 (11)

- January 2007 (11)

- December 2006 (12)

- November 2006 (16)

- October 2006 (13)

License

This work is licensed under a Creative Commons Attribution-Share Alike 3.0 United States License.

This has the feeling of Soros vs BOE all over again, yet with bigger stakes and even bigger players. But as I said last week, $400 billion for financial companies is a tidy sum, but they can withstand that - the real dominoes start when the fractional banking system works in reverse, pulling credit from an economy based on credit-growth, then causing positive feedback on economic cycle/bank earnings...Goldman will be updating that note in 3-6 months.

Ouch! Stoneleigh your hurting me fer sure %}

I'm sure you saw this from CR;

"Consumers Use the 401(k) ATM"

http://calculatedrisk.blogspot.com/2007/12/consumers-use-401k-atm.html

IMO this is the negative result of manipulation of the economic realities by TPTB.

I understand that they have to do what ever they can to avoid economic collapse, or at least appear to be doing so, but without the correct information people WILL make bad decisions like this.

I swear to buddha it looks more and more like this is being orchestrated.

One would like to think that at least some people realize what is going on and just plain cash in the retirement plans despite penalties and move them into inflation indexed treasuries or gold.

Unless these plans are invested exclusively in guaranteed treasuries, and almost none are, they will be worth little or nothing eventually. This does not even consider inflation and the possibility of withdrawals being blocked.

musashi, I agree that a few far-sighted folks may well take their futures into their own hands.

I'm vested in a Defined Pension Plan; up to a couple of years ago I was delighted that I had a benefit that's a dying breed. Now I feel the oposite. The managers bought whatever the brokerages were touting that month, which included SIV and subprime CDO paper. I can opt to self-direct my account, which lets me "choose" between a "growth mutual fund" or an annuity from an insurance company (which I'll bet is up to its eyeballs in "high yield" paper). No mention of gold or oil-service ETF's; I'm sure that's just an oversight that will be soon corrected...HAHAHAHAHA.

So now I'm doing ELP with a vengeance, as I've realized that my retirement is pretty much up to me.

PLAN, PLANt, PLANet

Errol in Miami

No need for orchestration, methinks.

With home equity withdrawals off the table, people have nowhere left to turn but plastic debt, of which we've seen countless stories and examples, and of course their pension provisions, of any shape and form that they can get their hands on.

I'm not familiar with the ins and outs of these plans and funds, but if it's anything like I presume it is, there's hefty premiums on early withdrawals.

The deepest tragedy lies in the cases where this "equity" is used merely to pay off mortgage and credit card debt.

The penalty typically is only 10%, and of course depending on the type of plan if the funds were not taxed going in then they are taxed as regular income. The penalty only applies for people younger then 59 1/2

There also are ways to make emergency withdrawals but for short periods and then they have to be paid back in.

If you withdraw on Jan 01 then the tax isn't due until 15 1/2 months later, but the banks may take some of it out up front to try and deter withdrawals.

People that go into retirement accounts to make payments on RE they can not afford are delusional, they will default later anyway in almost every case. These accounts are federally protected even in the case of bankruptcy and are the best (only?) hedge honest people that proceed in good faith have.

They dangle all these relief bills out there to give the middle class hope of a bailout if they can just hang in there long enough. It's a trap.

They will never help middle class people, there are no FEMA free money credit cards for the flooded cities in WA state, they are just trying to pick the middle class clean.

Bingo, I think we have a winner.

Couldn't agree more.

MEW, 401k, plastic... We still forgot one option:

If people default on the 396% interest loans, what then? Look for a rash of busted kneecaps and bodies turning up in rivers with feet encased in concrete.

I swear to buddha it looks more and more like this is being orchestrated.

Soup, Read this post from the previous Fin. RU.

(Read the whole article.)

http://canada.theoildrum.com/node/3355#comment-276849

John

Thanks Samsara - I read the snips the other day and intended to get to the whole article but...

Wow! I can't talk right now... just WOW!

I notice he is writing this from the relative safety of CHILE.

souperman, I second that WOW! Maund's analysis unfortunately fits the facts...

I'll also note that another wise macroeconomic writer, Enrico Orlandini, has chosen to live in Peru. I'm seeing a pattern here...

PLAN, PLANt, PLANet

It sort of dovetails with Ilargi's Goldman post below.

Goldman has (and had) undue influence over the Fed, Treasury and some foreign central banks. Their people are everywhere.

This much is a fact.

The question is where does Goldman's loyalty lie, and who pulls their strings.

Add the all powerful PAC that basically determines which candidates face off in the elections.

You tell me who is controlling the show.

You tell me who is controlling the show.

That's the over arching question isn't it?

I don't know, but I know more than I did a few years ago.

Here's a few clues. If nothing else if you digest all of this you will have no illusions on how money works or where it goes.

Enjoy, (sort of)

John

----------------------

First, Goldman Sachs and the Gov. There is NO daylight between them.

Sachs does Gov.

http://tinyurl.com/22dlpe

And THEIR bank, The Fed.

AMERICA'S FORGOTTEN WAR AGAINST THE CENTRAL BANKS

Here's a tid bit.

from 1929 to 1933 11,630 banks of the total of 26,401 in the United States to go bankrupt. This allowed central bankers to buy up rival banks and whole corporations at a deep discount.

It is interesting to note that biographies of J.P. Morgan, Joe F. Kennedy, J.D. Rockefeller and Bernard Baruch indicate that they all managed to transfer their assets out of the stock market and into gold just before the crash of 1929.

{Note the: 11,630 small family Savings and loans that became Fed banks.}

http://www.financialsense.com/fsu/editorials/dollardaze/2007/1020.html

Watch these video's on Money and The Fed.

Court Case involving the Fed.

http://www.silverbearcafe.com/private/criminal.html

Fed backers

http://www.silverbearcafe.com/private/rothschild.html

This one. Copy it to your disk. PDF warning. An incredible book of a LOT LOT of American History of the Fed.

The Secrets of the Federal Reserve

http://www.sandiego.indymedia.org/media/2007/02/125026.pdf

IMF / WORLD BANK DESTROYING COUNTRIES

http://www.unitypublishing.com/Government/IMF.htm

John F. Kennedy vs The Federal Reserve

http://www.silverbearcafe.com/private/JFK.html

Thanks for putting that together Samsara.

I had some of that but there are some real jewels in there.

Sure would like to get my hands on a copy of that USA Banker's Magazine, August 25 1924.

When does something like this go from being conspiracy theory to OMG come on everyone lets waste these effers?

And to add conspiracy to conspiracy, check this out from 2005...

And this goes to that for the NOC's in nationalist countries that actually work FOR their citizens it makes sense to withhold as much oil production as they can get away with.

Reminds me of Catherine Austin Fitts' discussion of the Red Button:

http://www.solari.com/articles/MoneyChangersInterview.htm

She argues that no one wants to stop unethical behavior (press the Red Button) because it would mean giving up our investments and pensions.

It never occurred to me until recently that TPTB would press the Red Button (stop the economy) in order to create Demand Destruction and slow down FF consumption.

It never occurred to me until recently that TPTB would press the Red Button (stop the economy)

World power consumption = population X rate of consumption

And

World power consumption (seems to) = World power production.

So if World power consumption is dropping due to less production, will the population be adjusted or will the rate of consumption be adjusted? Ya know - if there are TPTB who can bend things to their will for their convience?

how do the canadians here feel about a goldman alumnus set to take over as head of the central bank? time to dump the loonie for gold! oh wait, goldman just issued a short gold for 2008 recommendation. these are the same criminals hugely responsible for the mortgage mess, yet they claim to be perfectly hedged and have profited by shorting the subprime indices.

Not a good sign, but it was to be expected when we elected MonkeyBoy Jr.-on the positive side, we lucked out by not having him as our fearless leader when Condi was talking about Hussien turning NYC into a melting crater.

souperman2 said,

"I swear to buddha it looks more and more like this is being orchestrated."

I don't swear to buddha....but yeah, it's a whipped hysteria the likes of which is only possible in the internet era...as deepthroat said, "Follow the money."

You will see assets selling to the winners for a dime on the dollar once the blue and white collar schmoe's are shaken dry....

Years ago, I was told that to measure who had the power in a culture, look for the tallest buildings...the Egyptian priesthood had the pyramids, the Gothic priesthood had the Cathedrals, the Dutch began to surpass those with the "counting houses" of the Colonial traders....now look at any major city...

The tall towers belong to the financial services (misnomer that) and the medical community....

We are seeing a battle as to who can get to the boomers remaining money and investments...the biggest nest egg in history. At first, it looked like the medical community would get it....but the financial/banking community needed a way to get there first....break their investments down, and get the assets they have worked for on the cheap. They found it. Of course, many "post boomer" gen X and Y young are going to get caught up in the slaughter....but like the boomers in the 1970's, they have time in front of them....for the 45 plus year olds now, they (we, I should say) are running out of time.

These people will have to be VERY SHARP to avoid being driven into panic and making bad choices, or simply being confused by the media hysteria and panic machine, which is now working overtime. Let's admit it, we all will have to be VERY SHARP. This is a well organized attack, and will strike in ways that are as yet totally unexpected. Closer to TOD's agenda, those who have been amazed at the way in which "Peak Oil" has suddenly been embraced by the MSM....think about it. It now fits the agenda of the financial community.

But yeah, it's orchestrated so well it would make Leonard Bernstein jealous. :-)

RC

ThatsIt, it's too late for "These people will have to be VERY SHARP to avoid being driven into a panic and making bad choices..."

IMO they already made their bad choices. Rather than being panicked, they were seduced: into cash-out refies and 'investment' RE and SUV payments and credit card purchases of plasma TV's. They are now contractually obliaged to pay off that debt and bankruptcy has been "reformed". The trap is already sprung. The average 'consumer' can squirm around, or even chew off a leg (cash out the 401K), but trapped they are.

PLAN, PLANt, PLANet

Errol in Miami

...and bankruptcy has been "reformed".

With all the "HELP" the people, You Won't see them do anyything to the bankruptcy laws.

The minority bill to allow mortgage cram downs is outrageous.

It rewards criminal behavior and would totally lock up the economy as no one with a single active brain cell would ever loan a dime to anyone in the US again.

These POS are actually trying to break contract law that is as old as the ages.

The power of the sovereign is who ones turns to to enforce the contract. If the sovereign opts to not enforce, there is no contract....is there?

Sure. That's why they get "removed". It happened before.

The "Calculated Risk comment: Worse than August. Worse than 9/11." points to theoildrum.com.

Thanks - fixed.

When big finance announcements are delivered on a Friday after market close, something’s always wrong. Here’s a prime example. Canada non-bank ABCP has been dead (dare I say braindead) for 4 months, and at the deadline (sic), nothing’s been resolved. Not even the large write-downs already on the table (up to 50%, reportedly) are enough. Or the idea to turn short term ABCP (max: 270 days) into 9-year (!!) paper.

What to do now? Let’s say we agreed on a restructuring plan, and then in the same breath push the entire thing 3 more months ahead. That sounds positive, don't it? But we won't divulge any details, that'd spoil the jolly spirit. We'll claim confidentiality issues.

In the real world, we all know what it means: the paper still cannot be sold, unless, and that’s perhaps, at steep discounts. As in more than 50% below face value. We’ll all just keep hoping that the markets will revive. Problem is, we see one thing only out there: markets getting worse, not better.

Air Transat has turned heavy, and early, to the eggnog, we must assume: a 7% loss is very far removed from reality. One has to wonder why they do this. Then again, they did announce a 44% profit drop today. Could that be the reason?

The managers at Québec's largest pension fund, the Caisse, even though they're about to buy some more time, will not have a happy holiday season. They may be thinking of flying to the Caribean, never to return. Sooner or later a loss of $5-$10 billion must be made public. And the public won't like it.

Why does Transat take that ultra light write-down?

Maybe it’s just pieces falling together.

The aviation industry has a 1% profit margin, provided oil prices are $78 a barrel, with $190 billion in debt. And that is with heavily subsidized plane manufacturers, as in Boeing, Airbus, Embraer and Bombardier.

With banks reluctant to make loans, a 1% margin just won't cut it, one can safely assume. The risk of default is way too high.

Here's the recent trading activity for ABCP in Canada.

http://www.perimeterabcp.com/TradeHistory.aspx

The 'live' markets is equally exciting.

http://www.perimeterabcp.com/default.aspx

(It would be funnier if my employer didn't have >$350M in this stuff.)

Very impressive!

I thought I had mis-loaded the page because there were no transactions on it.. Then I got it.

Serious question then. If there are zero bids for this stuff, does that mean it is worth zero?

Or is there a "If I sell it, I will have to realise the loss - so I won't sell it" mentality here..?

One could have asked the same question in relation to some of the best farms in the US during the Great Depression, which were repossessed and put up for auction but received no bids. In an illiquid market, potential buyers don't want to risk bidding too much, and as value will likely fall over time they can afford to sit on the sidelines and wait.

Sellers probably wouldn't want to sell for what they might be offered now, and may well choose to hang on in the hope that the market will recover. Sellers resisting a 'haircut' are currently preventing agreement being reached on converting short term ABCP obligations to long term, even though this risks a firesale of assets that would result in much larger losses.

Of course the losses may well happen anyway - just ask Argentine bond holders from a few years ago. Converting short term bonds to long term and then defaulting on them later is not a new phenomenon.

Investor group misses debt deal deadline

The blame for that failure is put on Canadian banks' reluctance to accept part of the losses, but I think there's something else going on. The Canada non-bank ABCP has some peculiar quirks, it cedes much more to the swappers, the EU banks. That's why the Wall Street ratings agencies never rated it, only DBRS did. From Oct 1 2007:

This below is from Sep 28 2007.

What an insane mess, this ABCP thing. It's dead, accept it, you'd think. But then again, how do you explain to Québec's pensioners that you just lost them $20 billion?

No. You daren't. But it was funny.

Can you or anyone explain why the Canadian dollar is crashing vs US dollar last few weeks? Its gone from 1.11 to .98 (where it was a few months ago, true) but the same selloff hasn't occured with rest of $ basket.

Is it linked to canadian banks being worse off in this mess? I haven't followed closely enough.

That spike had no link to the real world, it was a flight from the USD towards whatever was available. Reality has set in now.

Canada is about to fall on its face real hard. Would anyone who reads our Round Ups still claim that Canada's economy is in such a superior position compared to the US? If so, we're not getting through. Canada depends on US consumers for over half its economic activity, I'd guesstimate.

For one, Canada has one lonesome claim to fame, being an energy superpower, but all of it goes slower and costlier than initially presumed. Yes, receding horizons. I'm on record saying that the oil sands will be dead by 2015, unless slave labor is introduced. No need to revise that one.

Canada's banks, as we will soon see, are not in good shape at all, and neither are its funds. The ABCP story in a good example of what is wrong over here. The two main pension funds, Ontario Teachers and the Caisse in Québec, have been competing for the best returns, and investing in tainted dirt to achieve them. That bell will soon toll. The same goes for pension funds worldwide. Being old will mean being very poor.

Canadian banks manage to do the brave face charade till now, but that won't last long. The CIBC finds it increasingly harder to hide away its mortgage losses, which will be substantial, but that's not its main problem, not even close. There's a much bigger monster lurking in that stocking, see below. My infallible eggnog hunch is the CIBC will fold next year, kind of like Canada's Citigroup, forcing other banks to expose themselves to the scrutiny of bright sunlight. And why would the CIBC be the only fool in the crowd?

Thank you.

I think the energy resources will prop up Canada vs US in future - but you are right - perhaps that energy is just too costly...lots of miles and lots of cold in between transport hubs...if tar sands is a bust - then what???

Maybe this is a silly question, but here goes: is it possible for the Fed itself to become insolvent? I had always believed the stories about 'Helicopter Ben' printing dollars to avoid deflation, but now I'm beginning to understand that the Fed can't do that - the Treasury creates dollars, the Fed creates credit. So if the Fed loans out money on collateral that later turns out to be worthless, can't they fold just like any other bank would? Or will the Treasury start cranking out REAL dollars to save them?

And many thanks to Stoneleigh and Ilargi for pulling all this together!

You're welcome, from both of us.

Actually, cranking out real dollars would sink them as it would devalue their holdings, which is one reason to suggest that printing real dollars is highly unlikely at this point. Another reason is that printing dollars would result in the US being caned in the bond market - not a choice an addict dependent on overseas borrowing is likely to make.

IMO we will see credit deflation and depression for a number of years, but following that we could well see the printing of actual dollars. IMO globalized financial markets are unlikely to have survived the shock, so international debt financing wouldn't be possible at that point anyway. I think capital controls we be reimposed over the next few years, and that the volume of trade will also fall substantially, as it did during the Depression.

Other than actual printed paper money we carry around in our wallets (which is a tiny fraction of all the dollars sloshing around the world) I didn't think the US government could actually create money. The govt is financed (almost?) entirely by tax receipts and borrowed money.

Virtually all the so called "money" in the modern world is really credit-based currency. The currency is created when banks make loans and destroyed when the loan is paid back or the borrower defaults. By manipulating the rates it charges banks, the Fed encourages/discourages banks from creating money by making loans. The Fed can create money directly by buying Treasuries. It probably has a few other tools for making money that I'm not aware of.

The Fed can also buy & sell gold, but I think that's fundamentally different because gold is a real asset. As an aside, it is an interesting question as to whether there is any gold left in Fort Knox, or whether the Fed & investors now own it all. I don't think there's ever been an accounting, and the Fed is never audited.

Wow. That is so wrong headed I don't know even where to begin.

Let's start with In the Beginning.